By Rick Clay

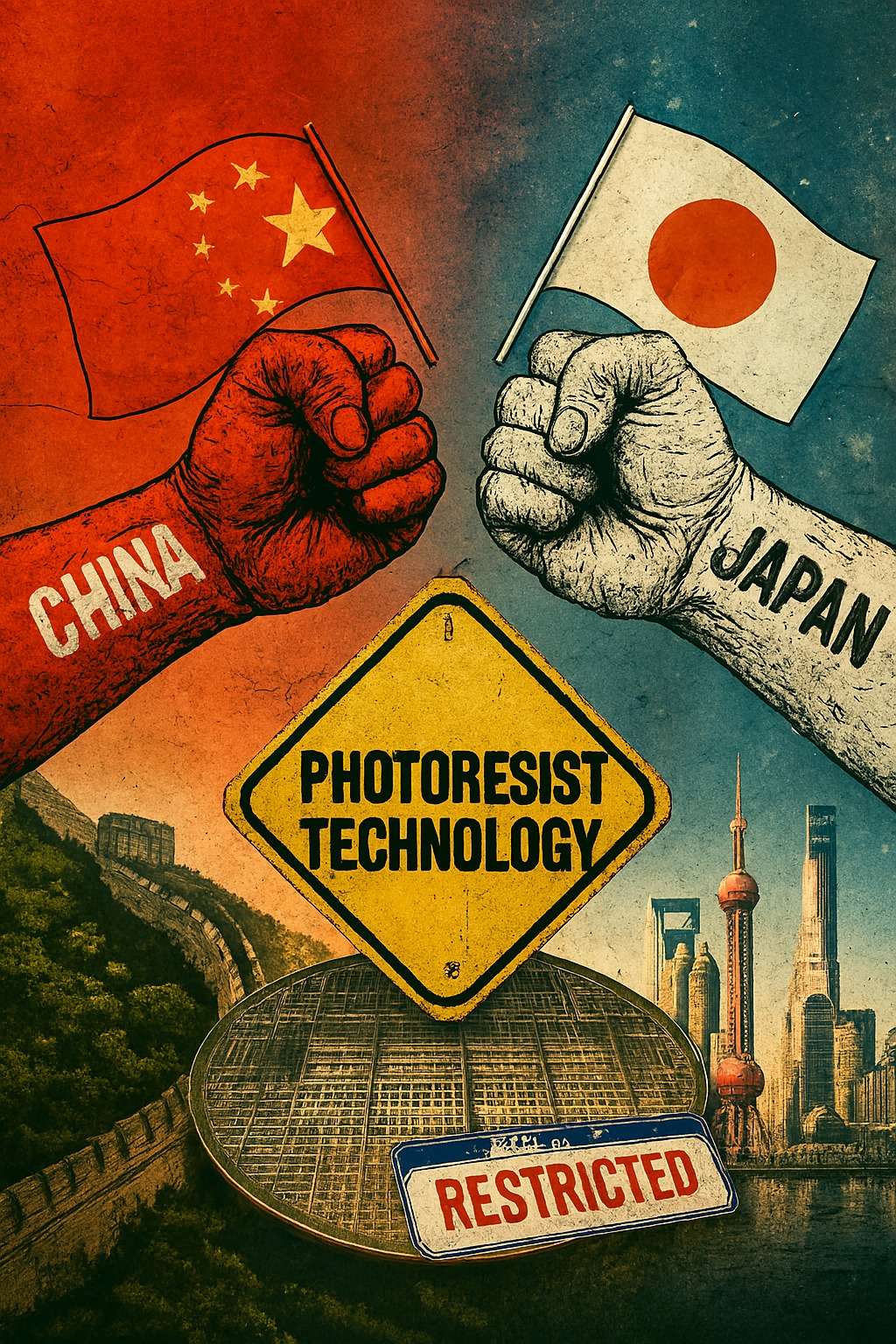

China’s semiconductor industry is entering a period of acute instability. Japan’s decision to restrict exports of photoresist a critical material for chipmaking—has left China’s fabs with only limited reserves, expected to last fewer than seven weeks. Without these imports, over 1,200 lithography machines could be idled, crippling production capacity. This crisis highlights the fragility of China’s “zombie companies,” firms that survive only through subsidies and debt rollovers. For U.S. policymakers and America First coalitions, this moment demonstrates the effectiveness of coordinated export controls and offers a strategic opportunity to reinforce industrial leadership while exposing China’s systemic weaknesses.

Background: Zombie Companies in China

Zombie companies are firms that cannot generate enough profit to cover debt interest payments, relying instead on bailouts or credit rollovers. In China, studies estimate that 20–30% of listed firms have exhibited zombie-like characteristics since the 2008 financial crisis. These firms are concentrated in industries such as steel, real estate, and semiconductors, where overcapacity and state intervention distort market signals. While some firms temporarily recover, many relapse into unprofitability, draining capital from productive enterprises. The International Monetary Fund has warned that zombie firms reduce overall productivity growth by crowding out investment and misallocating resources. In China’s case, they mask systemic weaknesses and create the illusion of industrial strength, while in reality they are dependent on state support.

Crisis Trigger: Japan’s Photoresist Ban

Japan’s Ministry of Economy, Trade and Industry announced new restrictions in 2025 on exports of semiconductor-related goods, including photoresist, lithography equipment, and advanced processors. Photoresist is indispensable in lithography, the process that etches circuits onto silicon wafers. Japan dominates this market, controlling nearly 90% of global supply, with companies like JSR, Tokyo Ohka Kogyo, and Shin-Etsu Chemical leading production. By halting shipments to China, Japan has effectively cut off the lifeline of Chinese chipmakers. Analysts estimate that China’s reserves will last six to seven weeks, after which production will grind to a halt. This move is part of a broader U.S.-led containment strategy, mirrored by similar restrictions from the Netherlands and the United States, targeting China’s access to advanced semiconductor technologies.

Consequences for China’s Semiconductor Sector.

The immediate impact is the risk of idling 1,200 lithography machines across China’s semiconductor fabs. While China has attempted to develop domestic lithography equipment, such as the 28nm machine by SMEE in 2025, these remain far behind global leaders like ASML’s EUV systems. Efforts to produce domestic photoresist have also failed to meet the precision required for advanced nodes. As a result, China’s electronics, defense, and AI industries face cascading disruptions. Semiconductors are central to China’s ambitions, with chips valued at over $150 billion in imports annually, making them China’s largest import category after oil. A prolonged disruption could cripple industries ranging from smartphones to military hardware, undermining both economic and strategic goals.

Strategic Implications for the U.S. and Allies.

This crisis demonstrates that tech containment works. Coordinated export controls by Japan, the U.S., and the Netherlands have effectively blocked China’s access to critical inputs, slowing its progress toward semiconductor independence. Zombie firms amplify the impact of these restrictions, as they lack the resilience to adapt without state support. For U.S. policymakers, this presents an opportunity to reinforce restrictions, incentivize reshoring of semiconductor production, and highlight China’s systemic weaknesses. By exposing the fragility of China’s industrial base, America and its allies can strengthen their own supply chains while reducing dependence on adversarial economies.

Coalition Messaging Recommendations

For coalition partners and investors, messaging should emphasize both the economic fragility of China and the effectiveness of coordinated policy measures. Investor briefs can highlight the risks of exposure to Chinese tech supply chains, particularly in semiconductors. Media campaigns should dramatize the crisis with visuals of idle factories, broken supply chains, and abandoned equipment. Policy advocacy should frame export controls not only as strategic necessities but also as moral imperatives to prevent authoritarian regimes from dominating critical technologies. By combining data-driven analysis with compelling imagery, coalitions can amplify the narrative of China’s economic decline and the resilience of America First strategies.

• Chart 1 (left): Japan’s photoresist market grows from $0.68B in 2025 to $1.45B by 2033, representing about 26% of the global market in 2025.

• Chart 2 (right): China’s 2025 import dependency highlights semiconductors at $150B annually, second only to oil imports at $250B.